When to Start Paying Taxes for Your Crypto Profits

It is that time of the year we all dread – the deadline to submit your tax returns and watch the digits in your bank account trickle into nothingness. This year, some of us should be concerned about this issue […]

It is that time of the year we all dread – the deadline to submit your tax returns and watch the digits in your bank account trickle into nothingness. This year, some of us should be concerned about this issue from an unprecedented angle – cryptocurrency taxes.

Last month, I wrote an article documenting how the IRS decided to crackdown on cryptocurrency profits by rectifying the 1031 loophole – the part of the tax code accounts for an exemption for ‘like kind exchanges’, which allows investors to swap assets that are of equal value without triggering a tax event. This is also known as the ‘1031 exchange’, and traders have always used it to exchange tangible property such as art or real estate without incurring any taxes. However, this loophole was amended last December, and starting Jan. 1, 2018, all cryptocurrency trades will be subjected to taxes, and this includes the exchanging of one cryptocurrency to another.

So, how does this affect me?

Before we dive into the nitty-gritty, we have to understand the difference between long-term and short-term capital gains, which depends on how long you owned the asset. Short-term capital gains tax rates are equal to your ordinary income tax. Long-term capital gains tax rates, which usually come into play on investments you’ve held for longer than a year, are much less onerous; many taxpayers qualify for a 0% tax rate.

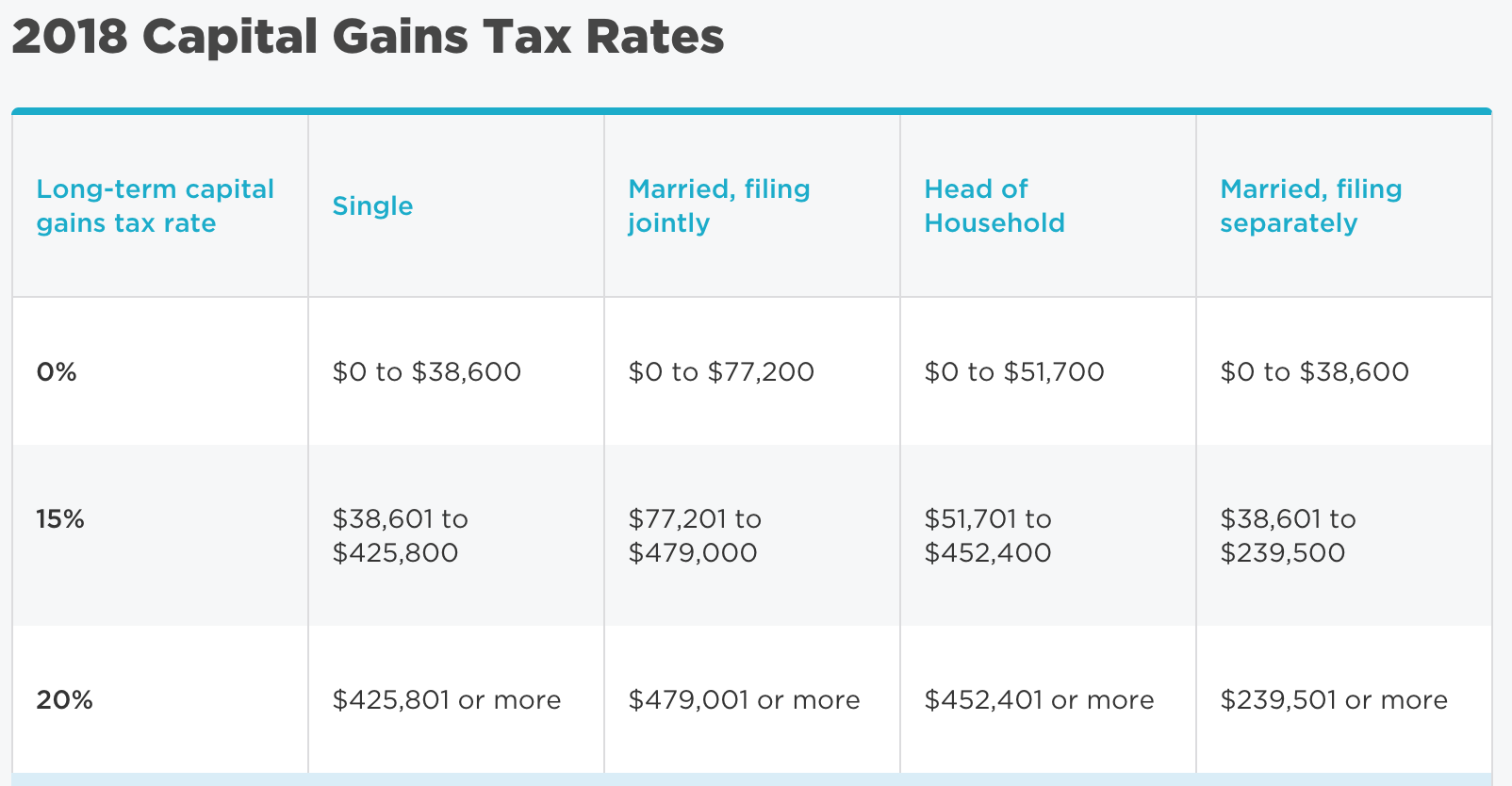

On Dec. 20, 2017, the Congress passed a sweeping overhaul of the U.S. tax code, with President Trump promising to sign it. The new rules do not change long-term capital gains tax rates themselves — for the 2018 tax year they’re 0%, 15% and 20%, the same as for 2017.

But the thresholds have changed.

Source: Nerdwallet

In other words, as long as you “HODL” your digital assets for over a year without cashing out on your profits, you will not have to pay taxes unless your profits are above $38,600.

It’s not that simple

Coming back to the amended 1031 loophole, you might still incur a taxable event even if you don’t formally cash out. Anyone using cryptocurrency to pay for goods or services must treat each purchase as a sale or even trading one cryptocurrency for another. I know there’s confusion over this treatment, but think of it like this: If you trade in your Amazon shares for Microsoft shares, that’s a taxable transaction, even if you don’t take cash out of your brokerage account. The same analysis applies to cryptocurrency trading – if you trade Ripple for Ethereum in order to buy other ERC20 tokens, that’s a taxable transaction.

Featured Image Source: Pinterest